Wisconsin 30 Index Outlook

Since the Trump administration took office on January 20th, one word has dominated trade and economic headlines. Tariffs. As a central pillar of the administration’s trade strategy, tariffs have been used both as a negotiating tool and a means of protecting domestic industries. Broad-based measures now include a 10% universal tariff on most imports and a steep 145% tariff on all Chinese goods, however, there has been a recent 90-day pause. While certain strategic exemptions have been granted, such as conditional relief for USMCA partners and exclusions for tech-related imports like smartphones and displays, the overall trade landscape remains volatile. Countries such as China, the EU, and Canada have responded with threats of WTO disputes and retaliatory tariffs, further amplifying global uncertainty. As firms struggle to navigate shifting criteria and unpredictable rate changes, tariffs have become a defining force in international trade policy and a major source of economic risk.

When analyzing the Wisconsin Index, 14 of the 30 companies (Figure 1) fall within the industrials sector, a group highly sensitive to tariffs and global trade disruptions. Due to their cyclical nature, industrials typically underperform during periods of economic uncertainty and slowing growth, making the index particularly vulnerable in the current tariff-heavy environment. This raises an important question: How did the Wisconsin Index respond during the first U.S.-China trade war, and what is it signaling now amid renewed tariff tensions? Understanding this performance history offers valuable insight into how the index may behave as trade policies continue to evolve.

Figure 1: Wisconsin Index Sectors

| Sector | Number of Companies |

|---|---|

| Industrials | 14 |

| Financials | 6 |

| Utilities | 3 |

| Consumer Discretionary | 2 |

| Information Technology | 2 |

| Healthcare | 1 |

| Materials | 1 |

| Consumer Staples | 1 |

The first U.S.-China trade war (2018–2019) was largely strategic and targeted, with tariffs aimed at specific sectors like steel, aluminum, and approximately $360 billion worth of Chinese imports. The Trump administration positioned these measures as leverage to address concerns over intellectual property theft, forced technology transfers, and longstanding trade imbalances. Although the tariffs were impactful, they were relatively focused in scope, and the overall economic disruption was limited where many companies were able to adapt through supply chain adjustments or passed costs on to consumers, resulting in less severe consequences than initially feared. However, let’s see how the Wisconsin Index, specifically industrials, performed during the first trade war (Figure 2).

Figure 2: Wisconsin Index Contribution to Returns (First Trade War)

![Contribution scatter plot by sector, 12/29/2017–12/31/2018. Most sectors cluster near the center. Industrials (circled in red) is the clear outlier, with roughly -25% total return and -7% contribution to return. Health Care and [Unassigned] are the top performers on the right.](https://uwm.edu/business/wp-content/uploads/sites/554/2026/04/imcp-figure-2-wi-index-contribution-to-return.jpg)

During the first trade war, the Wisconsin Index suffered significant losses, with 77% of its holdings, primarily from the Industrials, Financials, Materials, and Consumer Discretionary sectors, posting total returns worse than -15%. These sectors were particularly vulnerable to rising tariffs, supply chain disruptions, and weakening global demand, which eroded corporate earnings and investor confidence. The heavy concentration in cyclical industries made the index especially susceptible to macroeconomic shocks, highlighting the indexes economic sensitivity to international trade tensions.

Following the resolution of the trade war and toward the end of the COVID-19 pandemic, the Industrials sector experienced a strong rebound, driven by a resurgence in manufacturing and increased overall production. Pent-up consumer demand, government stimulus, and a renewed focus on domestic supply chains contributed to the sector’s growth. Companies ramped up capital expenditures, infrastructure spending picked up, and labor market conditions gradually improved, all of which helped fuel industrial output. This post-pandemic recovery phase marked a pivotal shift, as firms sought to localize production and reduce dependency on global supply chains, further strengthening the performance of industrial equities. As a result, the Wisconsin Index saw a significant boost, benefiting from its heavy exposure to industrial and cyclical sectors (Figure 3).

Figure 3: Wisconsin Index Contribution to Returns (Post First Trade War 12/30/2022 – 12/29/2023)

![Contribution scatter plot by sector, 12/30/2022–12/29/2023. Industrials (circled in red) is the standout performer, with roughly +20% total return and ~16% contribution to return. Most other sectors cluster near the bottom left with low contributions. [Unassigned] has the highest total return (~140%) but a more modest contribution (~5%).](https://uwm.edu/business/wp-content/uploads/sites/554/2026/04/imcp-figure-3-wi-index-contribution-to-return.jpg)

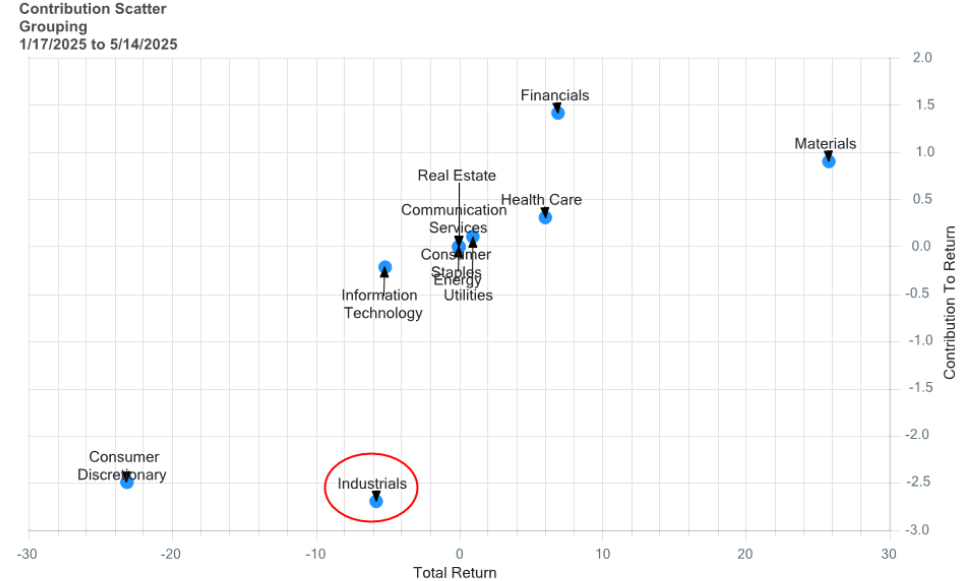

Looking back at the first trade war, followed by the subsequent recovery and now facing a new round of trade tensions, one might reasonably expect the Industrials sector to be underperforming significantly. However, that hasn’t been the case so far. The Industrials sector is currently posting a total return of approximately -5%, a relatively modest decline compared to roughly -20% experienced during the first trade war. This is particularly notable given that the current trade conflict is far more intense, broader in scope, and involves a wider range of countries (see Figure 9).This resilience raises several important questions. Are investors less concerned this time around because the initial trade war did not lead to a full-blown recession? Is there a belief that companies have since adapted to protectionist policies by diversifying supply chains or reshoring operations? Or perhaps the full economic impact of the new tariffs has yet to be realized, and markets are still underestimating the long-term consequences. It’s also possible that current macroeconomic conditions, such as strong labor markets, steady domestic demand, and fiscal support, are temporarily cushioning the blow. Still, the situation remains fluid, and Industrials could face renewed pressure if global trade frictions escalate or if delayed effects of the policy shift begin to surface more broadly in corporate earnings and capital investment.

Figure 4: Wisconsin Index Contribution to Returns (Second Trade War 1/17/2025 – 5/14/2025)

The Wisconsin Index’s journey through multiple economic cycles and trade conflicts reveals both its vulnerabilities and its capacity for resilience. Historically, its heavy exposure to Industrials and other cyclical sectors has left it susceptible to global trade disruptions, as seen during the first U.S.-China trade war. Yet the current environment, despite being defined by broader, more aggressive tariff measures, has not produced the same degree of underperformance. This change raises meaningful questions about whether companies and investors have become more adept at navigating protectionist policies, or whether the true economic fallout has simply been delayed.

While short-term fundamentals such as domestic demand, fiscal support, and strong labor markets appear to be cushioning the impact for now, the long-term trajectory of the Wisconsin Index will depend on how trade dynamics evolve, how companies adapt, and how global growth trends unfold. The current moment offers both risk and opportunity, and the coming year may serve as a critical test of the index’s structural strength and cyclical positioning.